Globally, digital revenue from advertising has risen from 14 per cent of total advertising revenue in 2009 to 25 per cent in 2013, and will hit 33 per cent by 2018. In contrast, digital consumer revenue in 2018 will account for just 17 per cent of the total amount consumers are expected to spend on media and entertainment. Meanwhile, non-digital advertising revenue will rise at a CAGR of only 1.9 per cent through the forecast period.

Adspend in China is a “complete digital story”, commented Marcel Fenez, global media and entertainment leader for PwC. “While there is monetary growth, the rate of growth in the other sectors will lose ground in the next five years.”

According to the report, China’s digital ad spend is expected to grow from 40 per cent in 2013 to 55 per cent of the total advertising pie in 2018. In comparison, TV is expected to shrink from 17 per cent to 13 per cent, newspapers from 20 per cent to 16 per cent and out of home media from 9 per cent to 5 per cent.

All other markets in Asia-Pacific are likewise expected to increase digital’s share of total ad spend. South Korea is expected to grow its digital share from 35 per cent in 2013 to 46 per cent in 2018, Australia from 30 per cent to 43 per cent and Singapore from 12 per cent to 18 per cent. Developing markets where digital advertising is still nascent are likewise expected to grow, albeit from a very low base. India is expected to grow from 6 per cent to 10 per cent, Indonesia from 1 per cent to 3 per cent and the Philippines from 4 per cent to 9 per cent.

Internet advertising

By 2018, internet advertising will be poised to overtake TV as the largest advertising segment globally. In 2009, internet advertising revenue was US$58.7 billion and TV advertising revenue was more than twice as big at $132.0 billion. But internet advertising revenue will rise at a 10.7 per cent CAGR to reach $194.5 billion in 2018, just $20 billion behind TV advertising.

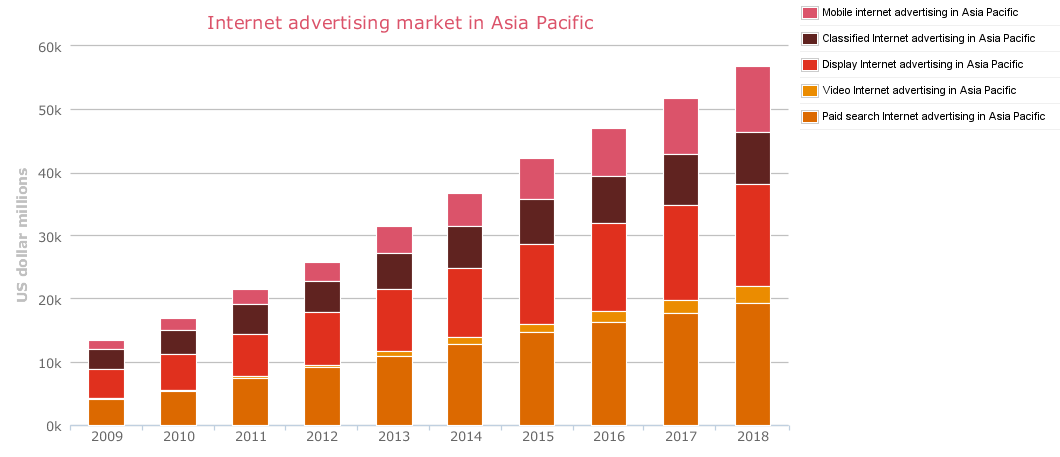

In Asia-Pacific, total internet advertising revenue was $31.4 billion in 2013, making it the world’s third-largest online ad region. Its revenue is forecast to grow at a CAGR of 12.6 per cent to reach $56.7 billion in 2018.

The region’s largest markets are China and Japan. Although almost equal in 2011—the Chinese market was worth $7.8 billion, the Japanese market $7.5 billion—the Chinese market has since pulled away, and by 2018, China will be comfortably the largest online ad market in Asia, worth $30.6 billion to Japan’s $10.8 billion.

The region’s largest markets are China and Japan. Although almost equal in 2011—the Chinese market was worth $7.8 billion, the Japanese market $7.5 billion—the Chinese market has since pulled away, and by 2018, China will be comfortably the largest online ad market in Asia, worth $30.6 billion to Japan’s $10.8 billion.

Other developing Asia-Pacific advertising markets will see huge rates of growth during the forecast period, but not to the extent where they will have a major impact on the region as a whole, according to PwC. In 2017, Australia and South Korea will remain the third- and fourth-largest markets in the Asia-Pacific region.

Paid search Internet advertising revenue is currently the largest online advertising medium in Asia-Pacific, worth $11.1 billion in 2013, having surpassed display in 2011. Search is expected to grow by a CAGR of 11.8 per cent to reach $19.3 billion, with its share of the online advertising market declining fractionally from 35 per cent to 34 per cent over the forecast period.

Display Internet advertising revenue is the second most popular format and takes a 31 per cent share of the market in 2013. The market, worth $9.7 billion in 2013, will grow at a CAGR of 10.6 per cent to reach $16.1 billion in 2018, representing 28 per cent of the total online advertising market. Although in many Asia-Pacific markets, search is a distant second place to online display advertising, search is dominant in the largest markets. It takes the lion’s share of spend in Australia and China, and while not the largest online ad medium in Japan, the country still adds a lot to search’s volume.

TV advertising

TV advertising revenues (including advertising on online TV properties) are continuing to grow worldwide and will expand by an average annual rate of 5.5 per cent until 2018. Including digital, TV advertising totalled $164.4 billion in 2013 and is expected to reach $214.7 billion in 2018. Excluding digital, TV revenue was $160.8 billion in in 2013 and is expected to reach $204.9 billion.

In other words, online TV advertising is a main driver of growth for traditional broadcasters. Revenue from traditional broadcasters in this space will increase from $3.7 billion in 2013 to $9.7 billion in 2018, and more than double its share of total TV advertising from 2.2 per cent in 2013 to 4.5 per cent in 2018. Traditional broadcasters still dominate and are adapting to the online video opportunity, so creating themselves a significant new revenue stream, despite competition from Internet rivals.

In other words, online TV advertising is a main driver of growth for traditional broadcasters. Revenue from traditional broadcasters in this space will increase from $3.7 billion in 2013 to $9.7 billion in 2018, and more than double its share of total TV advertising from 2.2 per cent in 2013 to 4.5 per cent in 2018. Traditional broadcasters still dominate and are adapting to the online video opportunity, so creating themselves a significant new revenue stream, despite competition from Internet rivals.

Asia-Pacific’s TV advertising market is expected to grow at a 5.8 per cent CAGR between 2013 and 2018 with revenues climbing from $39.7 billion to $52.7 billion. Terrestrial is the largest category making up 83.7 per cent of the total TV advertising revenues, although this will drop to 77.5 per cent in 2018. Indonesia, India, Pakistan and the Philippines will be the fastest-growing territories within the terrestrial category, all with a CAGR upwards of 7 per cent.

Interestingly, Thailand’s highly dominant TV market is expected to shrink in terms of ad spend share by three percentage points, from 59 per cent to 56 per cent. PwC's report does not take into account the recent coup, which is likely to negatively affect advertising spend for 2014 but should not badly affect the overall performance of the market over the next five years, explained Fenez.

Online advertising is the fastest-growing category in the region, with a CAGR of 53.6 per cent, albeit from a low base.

Newspapers

The drop in newspaper revenue has slowed from 10.9 per cent in 2009 to just 0.7 per cent in 2013.

“It’s interesting that while newspapers have been in free-fall in the world’s mature markets, the rate of decline is declining,” said Fenez. “It indicates that there is a natural plateau, which isn’t zero.”

Asia-Pacific continues to buck the trend however, with demand for newspapers continuing to grow. The average daily unit circulation of paid newspapers is up from 324.4 million in 2009 to 365.0 million in 2013. Although this growth was helped by the growth in cheap new titles, total newspaper circulation revenue also continued to grow, as did total newspaper advertising revenue.

Asia-Pacific continues to buck the trend however, with demand for newspapers continuing to grow. The average daily unit circulation of paid newspapers is up from 324.4 million in 2009 to 365.0 million in 2013. Although this growth was helped by the growth in cheap new titles, total newspaper circulation revenue also continued to grow, as did total newspaper advertising revenue.

In emerging economies, consumers welcome the chance to buy a newspaper as something that would not have been possible a generation ago. The growth of a new middle class across the region, notably in India and China, has created a new demand for newspapers, especially among the newly urban population.

“If you’ve always had to share a newspaper, being able to afford your own newspaper is something you want,” commented Fenez.

Although Japan remains one of the most important newspaper markets in the world, the circulation of newspapers is on a declining trend due to digitisation.

While individual countries’ newspaper markets across the region vary in their reliance on either advertising or circulation revenue, on a regional level, the industry’s revenue composition is split almost exactly down the middle. This can be a cause for comfort, ensuring that the sector is not overly exposed to a collapse in either single segment.

Mobile internet advertising

Global mobile internet advertising is expected to grow swiftly, although off a low base, from $14.1 billion in 2013 to $37.5 billion in 2018 at a CAGR of 21.5 per cent.

Global mobile internet advertising is expected to grow swiftly, although off a low base, from $14.1 billion in 2013 to $37.5 billion in 2018 at a CAGR of 21.5 per cent.

Asia-Pacific’s growth is nearly as swift in this sector with a CAGR of 20.2 per cent from 2013 ($4.1 billion) to 2018 ($10.3 billion).

“Although mobile internet advertising growth is swift, it’s fair to say that it isn’t easy,” noted Fenez. “People talk about it a lot, but we have to be realistic that it's hard to do. We're still trying to get to grips with what that means.”

Key takeaways

Consumer spending driven by experience

The opportunity for first-hand experience grows ever more valuable in a digital-saturated world. Consumers are spending most in the box-office when it comes to film, on live experiences for music and in trade shows for B2B.

“It’s a key thing that keeps coming through: Experience is really king,” said Fenez. “The strength of growth in box office, live music events and trade shows speaks to this. To me the story for growth is around experiential innovation. Innovation around the experience and relationships, targeting and innovation around delivery.”

Relationship innovation

Linked to the above trend is the need for businesses to look beyond digital innovation to target relationship innovation, recommends PwC’s report.

“Consumers' psychology has undergone a dramatic change," observed Fenez in the commentary he provides in the report's Outlook. "They've realised they can be at the centre of their own world of entertainment and media, switching from finding content experiences they have liked, to being found by content experiences they will like via every channel and device."

Relevance: now a target across all industries

Delivering such an experience demands more than crunching data: it means getting to know people as individuals, and them knowing you back. When this happens, the result is relevance, which brings the company that delivers it a disproportionate share of that individual's lifetime value, said the report.

It's not just entertainment and media businesses pursuing this opportunity. The battle for relevance is now being joined by participants ranging from utilities to retailers to carmakers, all competing head-on for the same relationships and all by offering the same level of personalisation and recommendations.

Fenez concluded his commentary with three behaviours to “build a successful strategy”:

Forging trust: Providing customers not just with relevant product and service experiences, but also full control over personal privacy. And embedding trust internally between everyone in the business.

Creating the confidence to move with speed and agility: Executing on new ideas quickly and decisively.

Empowering innovation: recognising past successes, while building on them for the future by innovating in ways unconstrained by that legacy.

The full report is available to PwC subscribers at www.pwcmediaoutlook.com

.jpg&h=334&w=500&q=100&v=20170226&c=1)

.jpeg&h=334&w=500&q=100&v=20170226&c=1)

.png&h=334&w=500&q=100&v=20170226&c=1)

.jpg&h=334&w=500&q=100&v=20170226&c=1)

.png&h=268&w=401&q=100&v=20170226&c=1)

.jpeg&h=268&w=401&q=100&v=20170226&c=1)